Phone: +86 21 51559030

contact@galleon.cc

Structural Core Materials Market worth 2.32 Billion USD by 2022

Jun 19,2018The global structural core materials market is projected to grow from USD 1.52 Billion in 2017 to USD 2.32 Billion by 2022, at a CAGR of 8.8%. Increase in the use of honeycomb structural core materials in the aerospace industry is expected to drive the structural core materials market. The aerospace industry has witnessed several changes in its components manufacturing in the past few decades. The use of wood and metal for manufacturing aircraft components has been replaced by various lightweight composites. Thus, the demand for structural core materials is increasing with the increasing penetration of composites in the aerospace industry.

The increasing number of patents filed for structural core materials by global players, growing manufacturing industries, and continuous agreements, partnerships & joint ventures, expansions, new product & technology launches, and mergers & acquisitions activities undertaken by various companies are key factors driving the global structural core materials market. Major factors fueling the growth of the structural core materials market are the growing demand from the wind energy industry, increasing usage of composites in the aerospace industry, and recovery of the marine sector in the US after the economic recession.

Based on type, the foam segment is estimated to lead the structural core materials market

Foam is the most common structural core material used in various applications due to its easy availability and low cost. Foam structural core materials are used in the sandwich construction of wind turbine blades, and they impart strength and stiffness while keeping the structure lightweight. PVC, PET, and SAN foams are the most popular structural core materials used in wind energy turbines. These foams are used in various applications, such as wind energy blades and nacelles, depending on their resin compatibility, temperature, manufacturing aspects, and costs. The demand for lightweight and fuel-efficient vehicles in the transportation industry is also driving the demand for foam. Moreover, they are used in various end-use industries, including marine.

Based on outer skin type, the GFRP segment is estimated to lead the structural core materials market

GFRP is a composite outer skin which is used in composite applications, especially in the wind energy, transportation, construction, and marine end-use industries. GFRP is mainly used in combination with balsa and PVC foam. GFRP panels provide a strong scratch resistant surface, chemical resistance, durability, and is lightweight. It is preferred over other building materials as it saves maintenance cost and is cheaper than other outer skins. Some of the major applications of GFRP includes wind blades, walls, and ceilings.

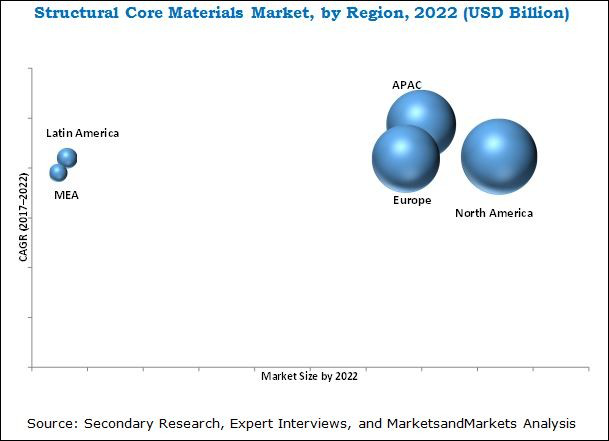

APAC is the key structural core materials market

In terms of volume, the APAC structural core materials market is projected to register the highest CAGR between 2017 and 2022, due to the increased demand for these materials from the wind energy and aerospace industries. In addition, easy availability of raw materials, low labor cost, growing manufacturing industries, new product developments, capacity expansions, and new plant establishments by various leading players are driving the structural core materials market in the region.

North America led the structural core materials market, in terms of value, in 2016, owing to high demand for honeycomb core materials from the aerospace and wind energy end-use industries. Established players, such as Hexcel Corporation (US) and The Gill Corporation (US) are accelerating their efforts to increase the production of honeycomb and foam core materials to meet the increasing demand from aircraft and wind blade manufacturers. Therefore, increasing application of honeycomb and foam core materials in the aerospace and wind energy end-use industries is expected to drive the structural core materials market.

Leading manufacturers of structural core materials are:

Diab Group (Sweden), Hexcel Corporation (US), Schweiter Technologies (Switzerland), Euro Composites (Luxembourg), Gurit Holding (Switzerland), The Gill Corporation (US), Changzhou Tiansheng New Materials Co. Ltd. (China), Plascore Incorporated (US), Armacell International (Luxembourg), and Evonik Industries (Germany). These players adopted various organic and inorganic developmental strategies between 2013 and 2017.

Diab Group (Sweden) is one of the major manufacturers of structural core materials, has already announced to participate in the upcoming 6th Annual China Aeronautical Materials and Process Summit (CAMPS 2018) as presentation sponsor. It emphasizes on excellence in consumer-centric product creation and focuses mainly on strategies, such as new product launches, agreements, partnerships, and expansions to grow. The company carried out continuous improvements in several business areas by maintaining its focus. It follows strategic moves to sustain its position as a market leader.

CAMPS is an annually event since year of 2012, which is a top management-gathering platform that officially hosted by Chinese Society of Aeronautics and Astronautics, supported by Chengdu Municipal Government, and co-organized AVIC Chengdu Aircraft Industrial (Group) Co., Ltd.,

CAMPS 2018 will be held to improve the efficiency and quality of manufacturing process experience through innovative technology and materials.

Register your interest or get in touch with marketing@galleon.cc for more details.

-

- © 2013 Galleon Corp. All Rights Reserved.